carolmusyoka consultancy

carolmusyoka consultancy

@carolmusyoka

@carolmusyoka

A man and his wife owned a very special goose. Every day the goose would lay a golden egg, which made the couple very rich.”Just think,” said the man’s wife, “If we could have all the golden eggs that are inside the goose, we could be richer much faster.”So, the couple killed the goose and cut her open, only to find that she was just like every other goose. She had no golden eggs inside of her at all, and they had no more golden eggs.

The Sunday Nation on March 4th 2018 published an article titled “New credit law to help small firms”. The article featured a debatable quote from the Member of Parliament for Kiambu constituency Mr Jude Njomo who shot to the national limelight with his successful Banking Act (Amendment) Bill 2015 that capped interest rates for Kenyan banks.Close to a year and a half later, with credit in the economy at an all time low and a significant drop in the profitability of the entire banking sector, Jude Njomo was quoted as saying,“The credit squeeze to SMEs is a deliberate effort by commercial banks to sabotage the economy so that the government may influence Parliament to remove the interest rate caps.”

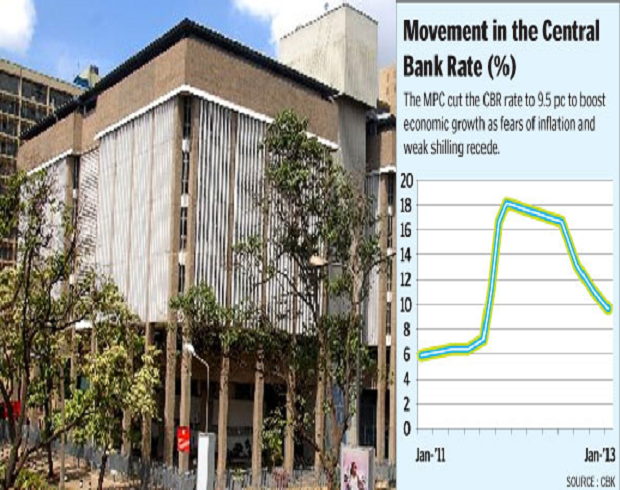

Parliament was about as smug as a bug in a rug when they passed the interest rate capping law. The collective view was that banks needed to be taught a lesson and to be dictated to on how to do business. However, the reverse happened. Banks simply stopped lending as it was not worth the risk and the funds that were meant to fuel the economy through lending for working capital and capital expenditure simply moved to the safest borrower of all mankind: the sovereign.

Mr. Jude Njomo and his legislative colleagues need to be disabused of one notion: You cannot juxtapose the word “banks” to the words “sabotage the economy” and expect a logical outcome. If anything, that is a fairly fallacious theory. It is about as oxymoronic as placing the words “parliament” next to the words “bans salary increases for lawmakers”. The two concepts are mutually dependent. Banks need a thriving economy to ensure that there is credit uptake and that those credit facilities are repaid which obviously leads to profitable business. Parliament need never set a ban for legislator salary increases because…well you can fill in the blanks yourself on that one. Aesop’s fable above summarizes it well, one does not kill the goose that lays the golden egg.

Credit is the lifeblood of any economy. Banks take in deposits and use the same to lend out to various sectors based on how much of their own capital they have in the business, what is termed as risk based capital allocation. Lending to the sovereign via treasury bills and bonds consumes minimal capital while lending to Tom, Dick and Harry consumes maximum capital. As banks by nature of regulatory rigour require a lot of capital, their shareholders will demand a significant return on that capital and lending to the ordinary mwananchi is the surest way of sweating that capital more efficiently. In a speech to the Kenya Bankers Association Banking Research Conference last September, the Central Bank Governor Patrick Njoroge reminded the banks about why they were in the position they were in. “There has (sic) been concerns about the Kenyan banking sector’s high average ROA of above 3% and ROE of close to 30%, when compared to similar economies….In any case the high ROAs and ROEs are not sustainable in the long term as customers cannot afford the high cost of banking services indefinitely.”

The Governor has been consistently rapping the knuckles of the Kenyan banking industry and the intervening period between the interest rate capping bill becoming law and its impending demise requires banks to significantly change their mindsets away from the traditional lending models to more innovative ways to make income as well as assess borrower repayment capacity (the fintechcredit algorithm methodologies for non-secured lending are a case in point). The Governorin his speech categorically pronounced the regulator as a key supporter of lenders that are fairly priced, lenders that provide differentiated risk-based pricing based on a borrower’s history and lenders that disclose information in a transparent manner. Legislators needs to be alive to the regulatory premise as the basis on which they should hold the banking industry to account, and not through reckless statements that the banking industry is in any shape or form killing its own economic golden goose.

Twitter: @carolmusyoka